Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

Buscar en scripts para "stop loss"

Long/Short/Exit/Risk management Strategy # LongShortExit Strategy Documentation

## Overview

The LongShortExit strategy is a versatile trading system for TradingView that provides complete control over entry, exit, and risk management parameters. It features a sophisticated framework for managing long and short positions with customizable profit targets, stop-loss mechanisms, partial profit-taking, and trailing stops. The strategy can be enhanced with continuous position signals for visual feedback on the current trading state.

## Key Features

### General Settings

- **Trading Direction**: Choose to trade long positions only, short positions only, or both.

- **Max Trades Per Day**: Limit the number of trades per day to prevent overtrading.

- **Bars Between Trades**: Enforce a minimum number of bars between consecutive trades.

### Session Management

- **Session Control**: Restrict trading to specific times of the day.

- **Time Zone**: Specify the time zone for session calculations.

- **Expiration**: Optionally set a date when the strategy should stop executing.

### Contract Settings

- **Contract Type**: Select from common futures contracts (MNQ, MES, NQ, ES) or custom values.

- **Point Value**: Define the dollar value per point movement.

- **Tick Size**: Set the minimum price movement for accurate calculations.

### Visual Signals

- **Continuous Position Signals**: Implement 0 to 1 visual signals to track position states.

- **Signal Plotting**: Customize color and appearance of position signals.

- **Clear Visual Feedback**: Instantly see when entry conditions are triggered.

### Risk Management

#### Stop Loss and Take Profit

- **Risk Type**: Choose between percentage-based, ATR-based, or points-based risk management.

- **Percentage Mode**: Set SL/TP as a percentage of entry price.

- **ATR Mode**: Set SL/TP as a multiple of the Average True Range.

- **Points Mode**: Set SL/TP as a fixed number of points from entry.

#### Advanced Exit Features

- **Break-Even**: Automatically move stop-loss to break-even after reaching specified profit threshold.

- **Trailing Stop**: Implement a trailing stop-loss that follows price movement at a defined distance.

- **Partial Profit Taking**: Take partial profits at predetermined price levels:

- Set first partial exit point and percentage of position to close

- Set second partial exit point and percentage of position to close

- **Time-Based Exit**: Automatically exit a position after a specified number of bars.

#### Win/Loss Streak Management

- **Streak Cutoff**: Automatically pause trading after a series of consecutive wins or losses.

- **Daily Reset**: Option to reset streak counters at the start of each day.

### Entry Conditions

- **Source and Value**: Define the exact price source and value that triggers entries.

- **Equals Condition**: Entry signals occur when the source exactly matches the specified value.

### Performance Analytics

- **Real-Time Stats**: Track important performance metrics like win rate, P&L, and largest wins/losses.

- **Visual Feedback**: On-chart markers for entries, exits, and important events.

### External Integration

- **Webhook Support**: Compatible with TradingView's webhook alerts for automated trading.

- **Cross-Platform**: Connect to external trading systems and notification platforms.

- **Custom Order Execution**: Implement advanced order flows through external services.

## How to Use

### Setup Instructions

1. Add the script to your TradingView chart.

2. Configure the general settings based on your trading preferences.

3. Set session trading hours if you only want to trade specific times.

4. Select your contract specifications or customize for your instrument.

5. Configure risk parameters:

- Choose your preferred risk management approach

- Set appropriate stop-loss and take-profit levels

- Enable advanced features like break-even, trailing stops, or partial profit taking as needed

6. Define entry conditions:

- Select the price source (such as close, open, high, or an indicator)

- Set the specific value that should trigger entries

### Entry Condition Examples

- **Example 1**: To enter when price closes exactly at a whole number:

- Long Source: close

- Long Value: 4200 (for instance, to enter when price closes exactly at 4200)

- **Example 2**: To enter when an indicator reaches a specific value:

- Long Source: ta.rsi(close, 14)

- Long Value: 30 (triggers when RSI equals exactly 30)

### Best Practices

1. **Always backtest thoroughly** before using in live trading.

2. **Start with conservative risk settings**:

- Small position sizes

- Reasonable stop-loss distances

- Limited trades per day

3. **Monitor and adjust**:

- Use the performance table to track results

- Adjust parameters based on how the strategy performs

4. **Consider market volatility**:

- Use ATR-based stops during volatile periods

- Use fixed points during stable markets

## Continuous Position Signals Implementation

The LongShortExit strategy can be enhanced with continuous position signals to provide visual feedback about the current position state. These signals can help you track when the strategy is in a long or short position.

### Adding Continuous Position Signals

Add the following code to implement continuous position signals (0 to 1):

```pine

// Continuous position signals (0 to 1)

var float longSignal = 0.0

var float shortSignal = 0.0

// Update position signals based on your indicator's conditions

longSignal := longCondition ? 1.0 : 0.0

shortSignal := shortCondition ? 1.0 : 0.0

// Plot continuous signals

plot(longSignal, title="Long Signal", color=#00FF00, linewidth=2, transp=0, style=plot.style_line)

plot(shortSignal, title="Short Signal", color=#FF0000, linewidth=2, transp=0, style=plot.style_line)

```

### Benefits of Continuous Position Signals

- Provides clear visual feedback of current position state (long/short)

- Signal values stay consistent (0 or 1) until condition changes

- Can be used for additional calculations or alert conditions

- Makes it easier to track when entry conditions are triggered

### Using with Custom Indicators

You can adapt the continuous position signals to work with any custom indicator by replacing the condition with your indicator's logic:

```pine

// Example with moving average crossover

longSignal := fastMA > slowMA ? 1.0 : 0.0

shortSignal := fastMA < slowMA ? 1.0 : 0.0

```

## Webhook Integration

The LongShortExit strategy is fully compatible with TradingView's webhook alerts, allowing you to connect your strategy to external trading platforms, brokers, or custom applications for automated trading execution.

### Setting Up Webhooks

1. Create an alert on your chart with the LongShortExit strategy

2. Enable the "Webhook URL" option in the alert dialog

3. Enter your webhook endpoint URL (from your broker or custom trading system)

4. Customize the alert message with relevant information using TradingView variables

### Webhook Message Format Example

```json

{

"strategy": "LongShortExit",

"action": "{{strategy.order.action}}",

"price": "{{strategy.order.price}}",

"quantity": "{{strategy.position_size}}",

"time": "{{time}}",

"ticker": "{{ticker}}",

"position_size": "{{strategy.position_size}}",

"position_value": "{{strategy.position_value}}",

"order_id": "{{strategy.order.id}}",

"order_comment": "{{strategy.order.comment}}"

}

```

### TradingView Alert Condition Examples

For effective webhook automation, set up these alert conditions:

#### Entry Alert

```

{{strategy.position_size}} != {{strategy.position_size}}

```

#### Exit Alert

```

{{strategy.position_size}} < {{strategy.position_size}} or {{strategy.position_size}} > {{strategy.position_size}}

```

#### Partial Take Profit Alert

```

strategy.order.comment contains "Partial TP"

```

### Benefits of Webhook Integration

- **Automated Trading**: Execute trades automatically through supported brokers

- **Cross-Platform**: Connect to custom trading bots and applications

- **Real-Time Notifications**: Receive trade signals on external platforms

- **Data Collection**: Log trade data for further analysis

- **Custom Order Management**: Implement advanced order types not available in TradingView

### Compatible External Applications

- Trading bots and algorithmic trading software

- Custom order execution systems

- Discord, Telegram, or Slack notification systems

- Trade journaling applications

- Risk management platforms

### Implementation Recommendations

- Test webhook delivery using a free service like webhook.site before connecting to your actual trading system

- Include authentication tokens or API keys in your webhook URL or payload when required by your external service

- Consider implementing confirmation mechanisms to verify trade execution

- Log all webhook activities for troubleshooting and performance tracking

## Strategy Customization Tips

### For Scalping

- Set smaller profit targets (1-3 points)

- Use tighter stop-losses

- Enable break-even feature after small profit

- Set higher max trades per day

### For Day Trading

- Use moderate profit targets

- Implement partial profit taking

- Enable trailing stops

- Set reasonable session trading hours

### For Swing Trading

- Use longer-term charts

- Set wider stops (ATR-based often works well)

- Use higher profit targets

- Disable daily streak reset

## Common Troubleshooting

### Low Win Rate

- Consider widening stop-losses

- Verify that entry conditions aren't triggering too frequently

- Check if the equals condition is too restrictive; consider small tolerances

### Missing Obvious Trades

- The equals condition is extremely precise. Price must exactly match the specified value.

- Consider using floating-point precision for more reliable triggers

### Frequent Stop-Outs

- Try ATR-based stops instead of fixed points

- Increase the stop-loss distance

- Enable break-even feature to protect profits

## Important Notes

- The exact equals condition is strict and may result in fewer trade signals compared to other conditions.

- For instruments with decimal prices, exact equality might be rare. Consider the precision of your value.

- Break-even and trailing stop calculations are based on points, not percentage.

- Partial take-profit levels are defined in points distance from entry.

- The continuous position signals (0 to 1) provide valuable visual feedback but don't affect the strategy's trading logic directly.

- When implementing continuous signals, ensure they're aligned with the actual entry conditions used by the strategy.

---

*This strategy is for educational and informational purposes only. Always test thoroughly before using with real funds.*

magic wand STSM"Magic Wand STSM" Strategy: Trend-Following with Dynamic Risk Management

Overview:

The "Magic Wand STSM" (Supertrend & SMA Momentum) is an automated trading strategy designed to identify and capitalize on sustained trends in the market. It combines a multi-timeframe Supertrend for trend direction and potential reversal signals, along with a 200-period Simple Moving Average (SMA) for overall market bias. A key feature of this strategy is its dynamic position sizing based on a user-defined risk percentage per trade, and a built-in daily and monthly profit/loss tracking system to manage overall exposure and prevent overtrading.

How it Works (Underlying Concepts):

Multi-Timeframe Trend Confirmation (Supertrend):

The strategy uses two Supertrend indicators: one on the current chart timeframe and another on a higher timeframe (e.g., if your chart is 5-minute, the higher timeframe Supertrend might be 15-minute).

Trend Identification: The Supertrend's direction output is crucial. A negative direction indicates a bearish trend (price below Supertrend), while a positive direction indicates a bullish trend (price above Supertrend).

Confirmation: A core principle is that trades are only considered when the Supertrend on both the current and the higher timeframe align in the same direction. This helps to filter out noise and focus on stronger, more confirmed trends. For example, for a long trade, both Supertrends must be indicating a bearish trend (price below Supertrend line, implying an uptrend context where price is expected to stay above/rebound from Supertrend). Similarly, for short trades, both must be indicating a bullish trend (price above Supertrend line, implying a downtrend context where price is expected to stay below/retest Supertrend).

Trend "Readiness": The strategy specifically looks for situations where the Supertrend has been stable for a few bars (checking barssince the last direction change).

Long-Term Market Bias (200 SMA):

A 200-period Simple Moving Average is plotted on the chart.

Filter: For long trades, the price must be above the 200 SMA, confirming an overall bullish bias. For short trades, the price must be below the 200 SMA, confirming an overall bearish bias. This acts as a macro filter, ensuring trades are taken in alignment with the broader market direction.

"Lowest/Highest Value" Pullback Entries:

The strategy employs custom functions (LowestValueAndBar, HighestValueAndBar) to identify specific price action within the recent trend:

For Long Entries: It looks for a "buy ready" condition where the price has found a recent lowest point within a specific number of bars since the Supertrend turned bearish (indicating an uptrend). This suggests a potential pullback or consolidation before continuation. The entry trigger is a close above the open of this identified lowest bar, and also above the current bar's open.

For Short Entries: It looks for a "sell ready" condition where the price has found a recent highest point within a specific number of bars since the Supertrend turned bullish (indicating a downtrend). This suggests a potential rally or consolidation before continuation downwards. The entry trigger is a close below the open of this identified highest bar, and also below the current bar's open.

Candle Confirmation: The strategy also incorporates a check on the candle type at the "lowest/highest value" bar (e.g., closevalue_b < openvalue_b for buy signals, meaning a bearish candle at the low, suggesting a potential reversal before a buy).

Risk Management and Position Sizing:

Dynamic Lot Sizing: The lotsvalue function calculates the appropriate position size based on your Your Equity input, the Risk to Reward ratio, and your risk percentage for your balance % input. This ensures that the capital risked per trade remains consistent as a percentage of your equity, regardless of the instrument's volatility or price. The stop loss distance is directly used in this calculation.

Fixed Risk Reward: All trades are entered with a predefined Risk to Reward ratio (default 2.0). This means for every unit of risk (stop loss distance), the target profit is rr times that distance.

Daily and Monthly Performance Monitoring:

The strategy tracks todaysWins, todaysLosses, and res (daily net result) in real-time.

A "daily profit target" is implemented (day_profit): If the daily net result is very favorable (e.g., res >= 4 with todaysLosses >= 2 or todaysWins + todaysLosses >= 8), the strategy may temporarily halt trading for the remainder of the session to "lock in" profits and prevent overtrading during volatile periods.

A "monthly stop-out" (monthly_trade) is implemented: If the lres (overall net result from all closed trades) falls below a certain threshold (e.g., -12), the strategy will stop trading for a set period (one week in this case) to protect capital during prolonged drawdowns.

Trade Execution:

Entry Triggers: Trades are entered when all buy/sell conditions (Supertrend alignment, SMA filter, "buy/sell situation" candle confirmation, and risk management checks) are met, and there are no open positions.

Stop Loss and Take Profit:

Stop Loss: The stop loss is dynamically placed at the upTrendValue for long trades and downTrendValue for short trades. These values are derived from the Supertrend indicator, which naturally adjusts to market volatility.

Take Profit: The take profit is calculated based on the entry price, the stop loss, and the Risk to Reward ratio (rr).

Position Locks: lock_long and lock_short variables prevent immediate re-entry into the same direction once a trade is initiated, or after a trend reversal based on Supertrend changes.

Visual Elements:

The 200 SMA is plotted in yellow.

Entry, Stop Loss, and Take Profit lines are plotted in white, red, and green respectively when a trade is active, with shaded areas between them to visually represent risk and reward.

Diamond shapes are plotted at the bottom of the chart (green for potential buy signals, red for potential sell signals) to visually indicate when the buy_sit or sell_sit conditions are met, along with other key filters.

A comprehensive trade statistics table is displayed on the chart, showing daily wins/losses, daily profit, total deals, and overall profit/loss.

A background color indicates the active trading session.

Ideal Usage:

This strategy is best applied to instruments with clear trends and sufficient liquidity. Users should carefully adjust the Your Equity, Risk to Reward, and risk percentage inputs to align with their individual risk tolerance and capital. Experimentation with different ATR Length and Factor values for the Supertrend might be beneficial depending on the asset and timeframe.

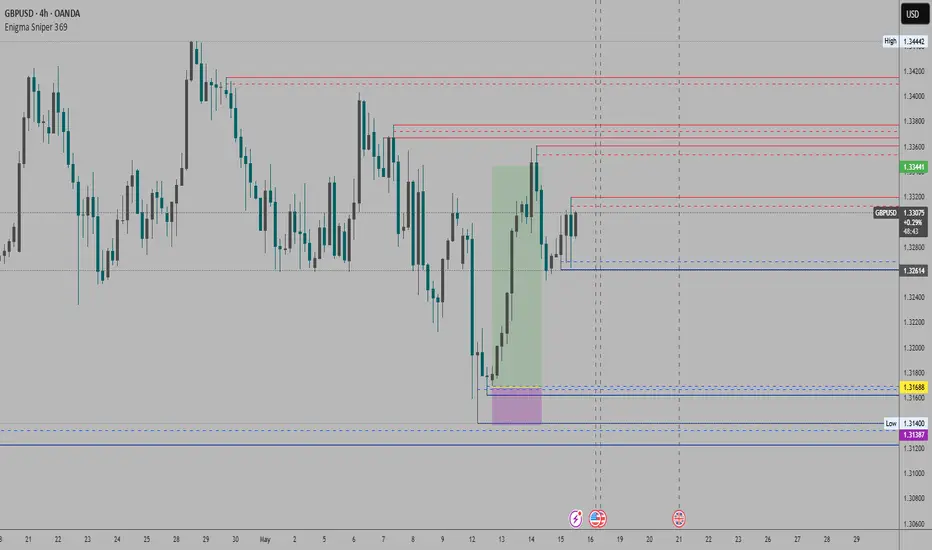

Enigma Sniper 369The "Enigma Sniper 369" is a custom-built Pine Script indicator designed for TradingView, tailored specifically for forex traders seeking high-probability entries during high-volatility market sessions.

Unlike generic trend-following or scalping tools, this indicator uniquely combines session-based "kill zones" (London and US sessions), momentum-based candle analysis, and an optional EMA trend filter to pinpoint liquidity grabs and reversal opportunities.

Its originality lies in its focus on liquidity hunting—identifying levels where stop losses are likely clustered (around swing highs/lows and wick midpoints)—and providing visual entry zones that are dynamically removed once price breaches them, reducing clutter and focusing on actionable signals.

The name "369" reflects the structured approach of three key components (session timing, candle logic, and trend filter) working in harmony to snipe precise entries.

What It Does

"Enigma Sniper 369" identifies potential buy and sell opportunities by drawing two types of horizontal lines on the chart during user-defined London and US

session kill zones:

Solid Lines: Mark the swing low (for buys) or swing high (for sells) of a trigger candle, indicating a potential entry point where stop losses might be clustered.

Dotted Lines: Mark the 50% level of the candle’s wick (lower wick for buys, upper wick for sells), serving as a secondary confirmation zone for entries or tighter stop-loss placement.

These lines are plotted only when specific candle conditions are met within the kill zones, and they are automatically deleted once the price crosses them, signaling that the liquidity at that level has likely been grabbed. The indicator also includes an optional EMA filter to ensure trades align with the broader trend, reducing false signals in choppy markets.

How It Works

The indicator’s logic is built on a multi-layered approach:

Kill Zone Timing: Trades are only considered during user-defined London and US session hours (e.g., London from 02:00 to 12:00 UTC, as seen in the screenshots). These sessions are known for high volatility and liquidity, making them ideal for capturing institutional moves.

Candle-Based Momentum Logic:

Buy Signal: A candle must close above its midpoint (indicating bullish momentum) and have a lower low than the previous candle (suggesting a potential liquidity grab below the previous swing low). This is expressed as close > (high + low) / 2 and low < low .

Sell Signal: A candle must close below its midpoint (bearish momentum) and have a higher high than the previous candle (indicating a potential liquidity grab above the previous swing high), expressed as close < (high + low) / 2 and high > high .

These conditions ensure the indicator targets candles that break recent structure to hunt stop losses while showing directional momentum.

Optional EMA Filter: A 50-period EMA (customizable) can be enabled to filter signals based on trend direction.

Buy signals are only generated if the EMA is trending upward (ema_value > ema_value ), and sell signals require a downward EMA trend (ema_value < ema_value ). This reduces noise by aligning entries with the broader market trend.

Liquidity Levels and Deletion Logic:

For a buy signal, a solid green line is drawn at the candle’s low, and a dotted green line at the 50% level of the lower wick (from the candle body’s bottom to the low).

For a sell signal, a solid red line is drawn at the candle’s high, and a dotted red line at the 50% level of the upper wick (from the body’s top to the high).

These lines extend to the right until the price crosses them, at which point they are deleted, indicating the liquidity at that level has been taken (e.g., stop losses triggered).

Alerts: The indicator includes alert conditions for buy and sell signals, notifying traders when a new setup is identified.

Underlying Concepts

The indicator is grounded in the concept of liquidity hunting, a strategy often employed by institutional traders. Markets frequently move to levels where stop losses are clustered—typically just beyond swing highs or lows—before reversing in the opposite direction. The "Enigma Sniper 369" targets these moves by identifying candles that break structure (e.g., a lower low or higher high) during high-volatility sessions, suggesting a potential sweep of stop losses. The 50% wick level acts as a secondary confirmation, as this midpoint often represents a zone where tighter stop losses are placed by retail traders. The optional EMA filter adds a trend-following element, ensuring entries are taken in the direction of the broader market momentum, which is particularly useful on lower timeframes like the 15-minute chart shown in the screenshots.

How to Use It

Here’s a step-by-step guide based on the provided usage example on the GBP/USD 15-minute chart:

Setup the Indicator: Add "Enigma Sniper 369" to your TradingView chart. Adjust the London and US session hours to match your timezone (e.g., London from 02:00 to 12:00 UTC, US from 13:00 to 22:00 UTC). Customize the EMA period (default 50) and line styles/colors if desired.

Identify Kill Zones: The indicator highlights the London session in light green and the US session in light purple, as seen in the screenshots. Focus on these periods for signals, as they are the most volatile and likely to produce liquidity grabs.

Wait for a Signal: Look for solid and dotted lines to appear during the kill zones:

Buy Setup: A solid green line at the swing low and a dotted green line at the 50% lower wick level indicate a potential buy. This suggests the market may have grabbed liquidity below the swing low and is now poised to move higher.

Sell Setup: A solid red line at the swing high and a dotted red line at the 50% upper wick level indicate a potential sell, suggesting liquidity was taken above the swing high.

Place Your Trade:

For a buy, set a buy limit order at the dotted green line (50% wick level), as this is a more conservative entry point. Place your stop loss just below the solid green line (swing low) to cover the full swing. For example, in the screenshots, the market retraces to the dotted line at 1.32980 after a liquidity grab below the swing low, triggering a buy limit order.

For a sell, set a sell limit order at the dotted red line, with a stop loss just above the solid red line.

Monitor Price Action: Once the price crosses a line, it is deleted, indicating the liquidity at that level has been taken. In the screenshots, after the buy limit is triggered, the market moves higher, confirming the setup. The caption notes, “The market returns and tags us in long with a buy limit,” highlighting this retracement strategy.

Additional Context: Use the indicator to identify liquidity levels that may be targeted later. For example, the screenshot notes, “If a new session is about to open I will wait for the grab liquidity to go long,” showing how the indicator can be used to anticipate future moves at session opens (e.g., London open at 1.32980).

Risk Management: Always set a stop loss below the swing low (for buys) or above the swing high (for sells) to protect against adverse moves. The 50% wick level helps tighten entries, improving the risk-reward ratio.

Practical Example

On the GBP/USD 15-minute chart, during the London session (02:00 UTC), the indicator identifies a buy setup with a solid green line at 1.32901 (swing low) and a dotted green line at 1.32980 (50% wick level). The market initially dips below the swing low, grabbing liquidity, then retraces to the dotted line, triggering a buy limit order. The price subsequently rises to 1.33404, yielding a profitable trade. The user notes, “The logic is in the last candle it provides new level to go long,” emphasizing the indicator’s ability to identify fresh levels after a liquidity sweep.

Customization Tips

Adjust the EMA period to suit your timeframe (e.g., a shorter period like 20 for faster signals on lower timeframes).

Modify the session hours to align with your broker’s timezone or specific market conditions.

Use the alert feature to get notified of new setups without constantly monitoring the chart.

Why It’s Useful for Traders

The "Enigma Sniper 369" stands out by combining session timing, momentum-based candle analysis, and liquidity hunting into a single tool. It provides clear, actionable levels for entries and stop losses, removes invalid signals dynamically, and aligns trades with high-probability market conditions. Whether you’re a scalper looking for quick moves during London open or a swing trader targeting session-based reversals, this indicator offers a structured, data-driven approach to trading.

ADX Breakout Strategy█ OVERVIEW

The ADX Breakout strategy leverages the Average Directional Index (ADX) to identify and execute breakout trades within specified trading sessions. Designed for the NQ and ES 30-minute charts, this strategy aims to capture significant price movements while managing risk through predefined stop losses and trade limits.

This strategy was taken from a strategy that was posted on YouTube. I would link the video, but I believe is is "against house rules".

█ CONCEPTS

The strategy is built upon the following key concepts:

ADX Indicator: Utilizes the ADX to gauge the strength of a trend. Trades are initiated when the ADX value is below a certain threshold, indicating potential for trend development.

Trade Session Management: Limits trading to specific hours to align with optimal market activity periods.

Risk Management: Implements a fixed dollar stop loss and restricts the number of trades per session to control exposure.

█ FEATURES

Customizable Stop Loss: Set your preferred stop loss amount to manage risk effectively.

Trade Session Configuration: Define the trading hours to focus on the most active market periods.

Entry Conditions: Enter long positions when the price breaks above the highest close in the lookback window and the ADX indicates potential trend strength.

Trade Limits: Restrict the number of trades per session to maintain disciplined trading.

Automated Exit: Automatically closes all positions at the end of the trading session to avoid overnight risk.

█ HOW TO USE

Configure Inputs :

Stop Loss ($): Set the maximum loss per trade.

Trade Session: Define the active trading hours.

Highest Lookback Window: Specify the number of bars to consider for the highest close.

Apply the Strategy :

Add the ADX Breakout strategy to your chart on TradingView.

Ensure you are using a 30-minute timeframe for optimal performance.

█ LIMITATIONS

Market Conditions: The strategy is optimized for trending markets and may underperform in sideways or highly volatile conditions.

Timeframe Specific: Designed specifically for 30-minute charts; performance may vary on different timeframes.

Single Asset Focus: Primarily tested on NQ and ES instruments; effectiveness on other symbols is not guaranteed.

█ DISCLAIMER

This ADX Breakout strategy is provided for educational and informational purposes only. It is not financial advice and should not be construed as such. Trading involves significant risk, and you may incur substantial losses. Always perform your own analysis and consider your financial situation before using this or any other trading strategy. The source material for this strategy is publicly available in the comments at the beginning of the code script. This strategy has been published openly for anyone to review and verify its methodology and performance.

Fibonacci Swing Trading BotStrategy Overview for "Fibonacci Swing Trading Bot"

Strategy Name: Fibonacci Swing Trading Bot

Version: Pine Script v5

Purpose: This strategy is designed for swing traders who want to leverage Fibonacci retracement levels and candlestick patterns to enter and exit trades on higher time frames.

Key Components:

1. Multiple Timeframe Analysis:

The strategy uses a customizable timeframe for analysis. You can choose between 4hour, daily, weekly, or monthly time frames to fit your preferred trading horizon. The high and low-price data is retrieved from the selected timeframe to identify swing points.

2. Fibonacci Retracement Levels:

The script calculates two key Fibonacci retracement levels:

0.618: A common level where price often retraces before resuming its trend.

0.786: A deeper retracement level, often used to identify stronger support/resistance areas.

These levels are dynamically plotted on the chart based on the highest high and lowest low over the last 50 bars of the selected timeframe.

3. Candlestick Based Entry Signals:

The strategy uses candlestick patterns as the only indicator for trade entries:

Bullish Candle: A green candle (close > open) that forms between the 0.618 retracement level and the swing high.

Bearish Candle: A red candle (close < open) that forms between the 0.786 retracement level and the swing low.

When these candlestick patterns align with the Fibonacci levels, the script triggers buy or sell signals.

4. Risk Management:

Stop Loss: The stop loss is set at 1% below the entry price for long trades and 1% above the entry price for short trades. This tight risk management ensures controlled losses.

Take Profit: The strategy uses a 2:1 risk-to-reward ratio. The take profit is automatically calculated based on this ratio relative to the stop loss.

5. Buy/Sell Logic:

Buy Signal: Triggered when a bullish candle forms above the 0.618 retracement level and below the swing high. The bot then places a long position.

Sell Signal: Triggered when a bearish candle forms below the 0.786 retracement level and above the swing low. The bot then places a short position.

The stop loss and take profit levels are automatically managed once the trade is placed.

Strengths of This Strategy:

Swing Trading Focus: The strategy is ideal for swing traders, targeting longer-term price moves that can take days or weeks to play out.

Simple Yet Effective Indicators: By only relying on Fibonacci retracement levels and basic candlestick patterns, the strategy avoids complexity while capitalizing on well-known support and resistance zones.

Automated Risk Management: The built-in stop loss and take profit mechanism ensures trades are protected, adhering to a strict 2:1 risk/reward ratio.

Multiple Timeframe Analysis: The script adapts to various market conditions by allowing users to switch between different timeframes (4hour, daily, weekly, monthly), giving traders flexibility.

Strategy Use Cases:

Retracement Traders: Traders who focus on entering the market at key retracement levels (0.618 and 0.786) will find this strategy especially useful.

Trend Reversal Traders: The strategy’s reliance on candlestick formations at Fibonacci levels helps traders spot potential reversals in price trends.

Risk Conscious Traders: With its 1% risk per trade and 2:1 risk/reward ratio, the strategy is ideal for traders who prioritize risk management in their trades.

BBTrend w SuperTrend decision - Strategy [presentTrading]This strategy aims to improve upon the performance of Traidngview's newly published "BB Trend" indicator by incorporating the SuperTrend for better trade execution and risk management. Enjoy :)

█Introduction and How it is Different

The "BBTrend w SuperTrend decision - Strategy " is a trading strategy designed to identify market trends using Bollinger Bands and SuperTrend indicators. What sets this strategy apart is its use of two Bollinger Bands with different lengths to capture both short-term and long-term market trends, providing a more comprehensive view of market dynamics. Additionally, the strategy includes customizable take profit (TP) and stop loss (SL) settings, allowing traders to tailor their risk management according to their preferences.

BTCUSD 4h Long Performance

█ Strategy, How It Works: Detailed Explanation

The BBTrend strategy employs two key indicators: Bollinger Bands and SuperTrend.

🔶 Bollinger Bands Calculation:

- Short Bollinger Bands**: Calculated using a shorter period (default 20).

- Long Bollinger Bands**: Calculated using a longer period (default 50).

- Bollinger Bands use the standard deviation of price data to create upper and lower bands around a moving average.

Upper Band = Middle Band + (k * Standard Deviation)

Lower Band = Middle Band - (k * Standard Deviation)

🔶 BBTrend Indicator:

- The BBTrend indicator is derived from the absolute differences between the short and long Bollinger Bands' lower and upper values.

BBTrend = (|Short Lower - Long Lower| - |Short Upper - Long Upper|) / Short Middle * 100

🔶 SuperTrend Indicator:

- The SuperTrend indicator is calculated using the average true range (ATR) and a multiplier. It helps identify the market trend direction by plotting levels above and below the price, which act as dynamic support and resistance levels. * @EliCobra makes the SuperTrend Toolkit. He is GOAT.

SuperTrend Upper = HL2 + (Factor * ATR)

SuperTrend Lower = HL2 - (Factor * ATR)

The strategy determines market trends by checking if the close price is above or below the SuperTrend values:

- Uptrend: Close price is above the SuperTrend lower band.

- Downtrend: Close price is below the SuperTrend upper band.

Short: 10 Long: 20 std 2

Short: 20 Long: 40 std 2

Short: 20 Long: 40 std 4

█ Trade Direction

The strategy allows traders to choose their trading direction:

- Long: Enter long positions only.

- Short: Enter short positions only.

- Both: Enter both long and short positions based on market conditions.

█ Usage

To use the "BBTrend - Strategy " effectively:

1. Configure Inputs: Adjust the Bollinger Bands lengths, standard deviation multiplier, and SuperTrend settings.

2. Set TPSL Conditions: Choose the take profit and stop loss percentages to manage risk.

3. Choose Trade Direction: Decide whether to trade long, short, or both directions.

4. Apply Strategy: Apply the strategy to your chart and monitor the signals for potential trades.

█ Default Settings

The default settings are designed to provide a balance between sensitivity and stability:

- Short BB Length (20): Captures short-term market trends.

- Long BB Length (50): Captures long-term market trends.

- StdDev (2.0): Determines the width of the Bollinger Bands.

- SuperTrend Length (10): Period for calculating the ATR.

- SuperTrend Factor (12): Multiplier for the ATR to adjust the SuperTrend sensitivity.

- Take Profit (30%): Sets the level at which profits are taken.

- Stop Loss (20%): Sets the level at which losses are cut to manage risk.

Effect on Performance

- Short BB Length: A shorter length makes the strategy more responsive to recent price changes but can generate more false signals.

- Long BB Length: A longer length provides smoother trend signals but may be slower to react to price changes.

- StdDev: Higher values create wider bands, reducing the frequency of signals but increasing their reliability.

- SuperTrend Length and Factor: Shorter lengths and higher factors make the SuperTrend more sensitive, providing quicker signals but potentially more noise.

- Take Profit and Stop Loss: Adjusting these levels affects the risk-reward ratio. Higher take profit percentages can increase gains but may result in fewer closed trades, while higher stop loss percentages can decrease the likelihood of being stopped out but increase potential losses.

[TTI] High Volume Close (HVC) Setup📜 ––––HISTORY & CREDITS––––

The High Volume Close (HVC) Setup is a specialised indicator designed for the TradingView platform used to identify specific bar. This tool was developed with the objective of identifying a technical pattern that trades have claimed is significant trading opportunities through a unique blend of volume analysis and price action strategies. It is based on the premise that high-volume bars, when combined with specific price action criteria, can signal key market movements.

The HVC is applicable both for swing and longer term trading and as a technical tool it can be used by traders of any asset type (stocks, ETF, crypto, forex etc).

🦄 –––UNIQUENESS–––

The uniqueness of the HVC Setup lies in its flexibility to determine an important price level based on historically important bar. The idea is to identify significant bars (e.g. those who have created the HIGHEST VOLUME: Ever, Yearly, Quarterly and meet additional criteria from the settings) and plot on the chart the close on that day as a significant level as well as theoretical stop loss and target levels. This approach allows traders to discern high volume bars that are contextually significant — a method not commonly found in standard trading tools.

🎯 ––––WHAT IT DOES––––

The HVC Setup indicator performs a series of calculations to identify high volume close bars/bar (HVC bars) based on the user requirements.

These bars are determined based on the highest volume recorded within a user-inputs:

👉 Period (Ever, Yearly, Quarterly) and must meet additional criteria such as:

👉 a minimum percentage Price Change (change is calculated based on a close/close) and

👉 specific Closing Range requirements for the HVC da.

The theory is that this is a significant bar that is important to know where it is on the chart.

The script includes a comparative analysis of the HVC bar's price against historical price highs (all-time, yearly, quarterly), which provides further context and significance to the identified bars. All of these USER input requirement are then taken into account as a condition to identity the High Volume Close Bar (HVC).

The visual representation includes color-coded bar (default is yellow) and lines to delineate these key trading signals. It then draws a blue line for the place where the close ofthe bar is, a red line that would signify a stop loss and 2 target profit levels equal to 2R and 3R of the risked level (close-stop loss). Additional lines can be turned on/off with their coresponding checkboxes in the settings.

If the user chooses "Ever" for Period - the script will look at the first available bar ever in Tradingview - this is generally the IPO bar;

If the users chooses "Yearly" - the script would look at the highest available bar for a completed year;

If the users chooses "Quarterly" - it would do the same for the quarter. (works on daily timeframe only);

While we have not backtested the performance of the script, this methodology has been widely publicised.

🛠️ ––––HOW TO USE IT––––

To utilize the HVC Setup effectively:

👉Customize Input Settings: Choose the HVC period, percentage change threshold, closing range, stop loss distance, and target multiples according to your trading strategy. Use the tick boxes to enable and disable if a given condition is used within the calculation.

👉Identify HVC Bars: The script highlights HVC bars, indicating potential opportunities based on volume and price action analysis.

👉Interpret Targets and Stop Losses: Use the color-coded lines (green for targets, red for stop losses) to guide your trade entries and exits.

👉Contextual Analysis: Always consider the HVC bar signals in conjunction with overall market trends and additional technical indicators for comprehensive trading decisions.

This script is designed to assist traders in identifying high-potential trading setups by using a combination of volume and price analysis, enhancing traditional methods with a unique, algorithmically driven approach.

Contrarian DC Strategy - w Entry SL Pause and TrailingStopDonchian Channel Setup:

The strategy uses a tool called the Donchian Channel. Imagine this as two lines (bands) on a chart that show the highest and lowest prices over a certain number of past trading days (default is 20 days).

There's also a centerline, which is the average of these two bands.

Entry Conditions for Trades:

Buying (Going Long): The strategy considers buying when the price touches or falls below the lower band of the Donchian Channel. However, this only happens if there has been a pause after a previous losing trade. This pause is a number of candles where no new trades are taken.

Selling (Going Short): Similarly, the strategy considers selling when price reaches or exceeds the upper band of the Donchian Channel. Again, this is subject to a pause after a losing trade.

Stop Loss and Take Profit:

Each trade has a "Stop Loss" and "Take Profit" set. The Stop Loss is a preset price level where the trade will close to prevent further losses if the market moves against your position. The Take Profit does the same but locks in profit if the market moves in your favor.

The Stop Loss is set based on a percentage of the price at which you entered the trade.

The Take Profit is determined by the Risk/Reward Ratio. This ratio helps balance how much you're willing to risk versus the potential reward.

Trailing Stop Loss:

When a trade is profitable, the strategy should involve a "Trailing Stop Loss." This means the Stop Loss level moves (or trails) the price movement to lock in profits as the market moves in your favor.

For a buy trade, if the price moves above the centerline of the Donchian Channel, the Trailing Stop Loss should be adjusted in the middle between the entry price and the centerline. Viceversa for a sell trade, it should be adjusted in the same way if the price goes below the centerline.

IMPORTANT: There's no allert for the trailing stop at the moment.

Post-Stop Loss Pause:

If a trade hits the Stop Loss (i.e., it's a losing trade), the strategy takes a break before opening another trade in the same direction. This pause helps to avoid entering another trade immediately in a potentially unfavorable market.

In summary, this strategy is designed to make trades based on the Donchian Channel, with specific rules for when to enter and exit trades, and mechanisms to manage risk and protect profits. It's contrarian because it tends to buy when the price is low and sell when the price is high, which is opposite to what many traders might do.

Narrow Range StrategyNarrow Range Strategy :

INTRODUCTION :

This strategy is based on the Narrow Range Day concept, implying that low volatility will generate higher volatility in the days ahead. The strategy sends us buy and sell signals with well-defined profit targets. It's a medium/long-term strategy. There's also a money management method that allows us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

NARROW RANGE (NR) DAY :

A Narrow Range Day is a day in which price variations are included in those of a specific day some time before. The high and low of this specific day form the "reference range". In general, we compare these variations with those of 4 or 7 days ago. The mathematical formula for finding an NR4 is :

If low > low(4) and high < high(4) :

nr = true

This implies that the current low is greater than the low of 4 days ago, and the current high is smaller than the high of 4 days ago. So today's volatility is lower than that of 4 days ago, and may be a sign of high volatility to come.

PARAMETERS :

Narrow Range Length : Corresponds to the number of candles back to compare current volatility. The default is 4, allowing comparison of current volatility with that of 4 candles ago.

Stop Loss : Percentage of the reference range on which to set an exit order to limit losses. The minimum value is 0.001, while the maximum is 1. The default value is 0.35.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by an amount chosen by the user.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot was used to test NR4 and NR7 with all possible Stop Losses in order to find out which combination generates the highest return on BITSTAMP:ETHUSD while limiting the drawdown. This strategy is the most optimal with an NR4 and a SL of 35% of the reference range size in 5D timeframe.

BUY AND SHORT SIGNALS :

When an NR is spotted, we create two stop orders on the high and low of the reference range. As soon as there's a breakout from this reference range (shown in blue on the chart), we open a position. We're LONG if there's a breakout on the high and SHORT if there's a breakout on the low. Executing a stop order cancels the second stop order.

RISK MANAGEMENT :

This strategy is subject to losses. We manage our risk with Stop Losses. The user is free to enter a SL as a percentage of the reference range. The maximum amount risked per trade therefore depends on the size of the range. The larger the range, the greater the risk. That's why we have set a maximum Stop Loss to 10% to limiting risks per trade.

The special feature of this strategy is that it targets a precise profit objective. This corresponds to the size of the reference range at the top of the high if you're LONG, or at the bottom of the low if you're short. In the same way, the larger the reference range, the greater the potential profits.

The risk reward remains the same for all trades and amounts to : 100/35 = 2.86. If the reference range is too high, we have set a SL to 10% of the trade value to limit losses. In that case, the risk reward is less than 2.86.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

NOTE :

Please note that the strategy is backtested from 2017-01-01. As the timeframe is 5D, this strategy is a medium/long-term strategy. That's why only 37 trades were closed. Be careful, as the test sample is small and performance may not necessarily reflect what may happen in the future.

Enjoy the strategy and don't forget to take the trade :)

Supertrend, MA 44|6, EMA FIBS 13|21|34I have this indicator based on my strategy. This indicator is based on existing functions available in the system. I haven't added anything new. This indicator uses Supertrend, MA44|6, EMA fibs 13|21|34 combining to find a profitable trade.

- Supertrend : Indicator uses supertrend strategy with default ATR period of 10 and Factor value 3. These values can be customized based on your preferences. Uptrend is denoted by green color and downtrend by red color. You can change the colors based on your preferences.

- MA 44|6: Indicator plots moving averages of 44 and 6. These values can be customized based on your preferences. Although it is highly recommended to keep 44 as is. Value 6 can be adjusted based on your preference. Default color for uptrend is green and for downtrend is red. You can change the colors based on your preferences.

- FIBS EMA 13|21|34: Indicator plots EMA of fibbonacci numbers 13, 21,34 to identify consolidation and breakout. The periods can be adjusted but it is highly recommended not to do so. Default colors for 13,21 and 34 is Aqua, Blue and Navy respectively. You can change the colors based on your preferences.

When to take trade?

To take a trade all conditions needs to be fulfilled.

Supertrend : Always take a trade in the direction of Supertrend. It is always advisable to take trade if the trend is changing or price is taking support of resistance.

MA 44|6: Moving average 44 indicates average price of 44 last candles and 6 for last 6 candles. Price crossing MA 44 indicates change in trend. It is advisable to take trade at crossing the line above or below. If many candles closing near MA 44 then it indicates consolidation. The more far the candle closes from MA44 the better. MA 6 is used to identify when to enter or exit the trade. If candle closes away from MA 6 then you can wait for candle to start near the MA 6 line. If candle closes above/below MA 6 you can exit your trade.

Fibonacci 13|21|34: When all lines are closed it indicates consolidation. When price breakouts to either direction you can take a trade in that direction with following conditions.

Bullish Trade:

When to enter?

If candle closed above MA 44, Supertrend is uptrend and EMA Fibs are moving away and are above MA 44. The price is near to MA 6 line then you can enter into bullish trade. If price is away from MA 6 then you should wait until the price/line comes near to avoid loss.

When to exit?

Price moving in opposite direction:

You should set a stop loss when you enter the trade. The stop loss can be set below the low of the previous candle or any other strategy you have. But it is really important to set the stop loss. If price moves in opposite direction then your stop loss will hit and you will be out of the trade.

Price moving in same direction:

Once you enter the trade you can exit based on two conditions whichever suits you.

1. Exit the trade if candle closes below MA6. The drawback is you may exit too early. You can also adjust the period based on your preferences.

2. Exit the trade if candle closed below low of previous candle. The drawback is you may book less profit but you can capture the movement very well.

Bearish Trade:

When to enter?

If candle closed below MA 44, Supertrend is downtrend and EMA Fibs are moving away and are below MA 44. The price is near to MA 6 line then you can enter into bearish trade. If price is away from MA 6 then you should wait until the price/line comes near to avoid loss.

When to exit?

Price moving in opposite direction:

You should set a stop loss when you enter the trade. The stop loss can be set below the low of the previous candle or any other strategy you have. But it is really important to set the stop loss. If price moves in opposite direction then your stop loss will hit and you will be out of the trade.

Price moving in same direction:

Once you enter the trade you can exit based on two conditions whichever suits you.

1. Exit the trade if candle closes below MA6. The drawback is you may exit too early. You can also adjust the period based on your preferences.

2. Exit the trade if candle closed below low of previous candle. The drawback is you may book less profit but you can capture the movement very well.

When not to take trade?

1. If MA 44 is completely horizontal and EMA Fibs are very close to each other. This indicates that the market is consolidated and if you enter the trade you may hit stop loss very often.

Note: Please note that I am not expert and I don't take any responsibility of your profits or losses. I have created this indicator based on my knowledge and it is for study purpose. Use of this indicator is totally your responsibility. Use all your knowledge and expertise and don't totally depend on the indicator. Don't forget to use stop loss and do money management.

Happy Trading!

Hooke's Law: Market ElasticityHooke's Law: Market Elasticity is a physics-based mean reversion system that models price action using the principles of Classical Mechanics.

Most technical indicators treat the market as a purely statistical entity. This script takes a different approach, treating the market as a physical object with Mass (Volume) and Stiffness (Volatility) . By adapting Hooke’s Law of Elasticity (𝐹=−𝑘𝑋), it visualizes the "Tensile Stress" between price and its equilibrium, identifying the exact moment when a trend becomes unsustainable and must "snap back."

The Physics of Trading

In physics, Hooke's Law states that the force needed to extend a spring is proportional to the distance it is stretched. We map this to financial markets using four key components:

Equilibrium (𝑋=0): The "Resting State" of the market, calculated using a Volume-Weighted Moving Average (VWMA) . This represents the fair value where buyers and sellers agree.

2. Displacement (𝑋): The distance price travels away from this equilibrium.

3. Spring Constant (𝑘): We use Volatility (Standard Deviation) to measure the market's "stiffness."

• Low Volatility: The spring is loose; price can wander far without snapping.

• High Volatility: The spring is stiff; even small deviations create massive tension.

4. Force (𝐹): The calculation is weighted by Relative Volume . A price spike on low volume has low force (easy to reverse), while a spike on high volume carries high momentum (harder to reverse).

Visual Guide & Signals

The indicator uses a hierarchy of visuals to guide you through the trade lifecycle:

1. The Elastic Ribbon (Heatmap)

Connects Price to the Baseline. As the ribbon turns Solid White , the market has reached its Elastic Limit (Critical Zone). This is your warning that a move is overextended.

2. The "Golden" Labels (LONG / SHORT)

These are your Entry Signals . They appear only when the physics "snap" is confirmed by an internal momentum filter and price action.

3. The Small Circles (Minor Reversions)

These dots represent "Minor Snaps." They occur when the elastic tension releases, but the momentum filter hasn't fully confirmed a major reversal.

• Usage: These are excellent Early Warning signs or Scale-In points for aggressive traders.

Strategy: Entries, Exits & Take Profits

This script is designed as a complete system. Here is how to manage the trade using the visual cues:

• Entry: Wait for a LONG or SHORT label to appear.

• Stop Loss: Use the Solid White Line that appears automatically with the signal. If price touches this line, the physics setup has failed—exit immediately.

• Take Profit 1 (The Equilibrium): The Gray Baseline represents the market's center of gravity. In mean reversion trading, price tends to snap back to this line. This is the statistically highest-probability target.

• Take Profit 2 (The Circles): If you are in a trade and a Circle appears in the opposite direction, it indicates the market is experiencing counter-tension. This is an ideal place to secure partial profits or trail your stop.

Settings & Configuration

• Baseline Length (Default: 34): The lookback period for the Center of Gravity.

• Elasticity Limit (Default: 2.618): The Golden Ratio is used as the standard deviation threshold for the "Critical Zone."

• Volume Weighting (Default: True): Recommended. Adds the "Mass" component to the physics calculation.

• Stop Loss Buffer (Default: 0.5): The distance (in Sigma) for the Stop Loss placement.

Risk Disclaimer

Not Financial Advice: This indicator is designed for educational and analytical purposes only. It visualizes market data based on mathematical formulas (Hooke's Law and Statistical Deviation) and does not guarantee future performance or profits.

Market Risks: Financial trading involves significant risk. The "Critical Zones" and "Signals" generated by this script identify statistical extremes, but markets can remain irrational or overextended for long periods ("Plastic Deformation").

Usage: Do not trade blindly based on these signals. Always use this tool in conjunction with your own analysis, risk management, and stop-losses. The author assumes no responsibility for any trading losses incurred while using this script.

Mean-Reversion with CooldownThis strategy requires no indicators or fundamental analysis. It is designed for longer-term positions and works especially well on unleveraged instruments with strong long-term upward trends, such as precious metals. Feel free to experiment with different timeframes — I’ve found that 1-hour charts work particularly well for cryptocurrencies.

The idea is to filter out ongoing bear phases as effectively as possible and capitalize on long-term bull runs.

The script implements an idea that came to me in a state of complete sleep deprivation: open a random long position with a fixed take-profit (TP) and a tight stop-loss (SL).

If the TP is hit — great, we simply try again.

If the SL is triggered — too bad, we pause for a while and then try again.

## Cooldown (Waiting) Mechanism

The waiting mechanism is simple: the more consecutive SL hits we get, the longer we wait before opening the next trade. The waiting time is measured in closed candles, and thus depends on the timeframe you are using.

## Two cooldown calculation modes are currently supported:

### 1. FIBONACCI

The cooldown follows the Fibonacci sequence, based on the number of consecutive losses:

1st loss → wait 1 bar

2nd loss → wait 1 bar

3rd loss → wait 2 or 3 bars (depending on definition)

4th loss → wait 3 or 5 bars

etc.

### 2. POWER OF TWO

The cooldown increases exponentially:

1st loss → wait 2 bars

2nd loss → wait 4 bars

3rd loss → wait 8 bars

4th loss → wait 16 bars

and so on, using the formula 2ⁿ.

## Configurable Parameters

### Cooldown Pause Calculation

The settings allow you to define the SL and TP as percentages of the position value.

The "Cooldown Pause Calculation" option determines how the next cooldown duration is computed after a losing trade.

The system keeps track of how many consecutive losses have occurred since the last profitable trade. That counter is then used to compute how many bars we must wait before opening the next position.

### Maximum Cooldown

The "Max Cooldown Candles" setting defines the maximum number of bars we are allowed to wait before placing a new trade. This prevents the strategy from “locking itself out” for too long and mitigates the fear of missing out (FOMO).

Once the cooldown duration reaches this maximum, the system essentially wraps around and starts the progression again. In the script, this is handled using a simple modulo operation based on the chosen maximum.

Mars Signals - Ultimate Institutional Suite v3.0(Joker)Comprehensive Trading Manual

Mars Signals – Ultimate Institutional Suite v3.0 (Joker)

## Chapter 1 – Philosophy & System Architecture

This script is not a simple “buy/sell” indicator.

Mars Signals – UIS v3.0 (Joker) is designed as an institutional-style analytical assistant that layers several methodologies into a single, coherent framework.

The system is built on four core pillars:

1. Smart Money Concepts (SMC)

- Detection of Order Blocks (professional demand/supply zones).

- Detection of Fair Value Gaps (FVGs) (price imbalances).

2. Smart DCA Strategy

- Combination of RSI and Bollinger Bands

- Identifies statistically discounted zones for scaling into spot positions or exiting shorts.

3. Volume Profile (Visible Range Simulation)

- Distribution of volume by price, not by time.

- Identification of POC (Point of Control) and high-/low-volume areas.

4. Wyckoff Helper – Spring

- Detection of bear traps, liquidity grabs, and sharp bullish reversals.

All four pillars feed into a Confluence Engine (Scoring System).

The final output is presented in the Dashboard, with a clear, human-readable signal:

- STRONG LONG 🚀

- WEAK LONG ↗

- NEUTRAL / WAIT

- WEAK SHORT ↘

- STRONG SHORT 🩸

This allows the trader to see *how many* and *which* layers of the system support a bullish or bearish bias at any given time.

## Chapter 2 – Settings Overview

### 2.1 General & Dashboard Group

- Show Dashboard Panel (`show_dash`)

Turns the dashboard table in the corner of the chart ON/OFF.

- Show Signal Recommendation (`show_rec`)

- If enabled, the textual signal (STRONG LONG, WEAK SHORT, etc.) is displayed.

- If disabled, you only see feature status (ON/OFF) and the current price.

- Dashboard Position (`dash_pos`)

Determines where the dashboard appears on the chart:

- `Top Right`

- `Bottom Right`

- `Top Left`

### 2.2 Smart Money (SMC) Group

- Enable SMC Strategy (`show_smc`)

Globally enables or disables the Order Block and FVG logic.

- Order Block Pivot Lookback (`ob_period`)

Main parameter for detecting key pivot highs/lows (swing points).

- Default value: 5

- Concept:

A bar is considered a pivot low if its low is lower than the lows of the previous 5 and the next 5 bars.

Similarly, a pivot high has a high higher than the previous 5 and the next 5 bars.

These pivots are used as anchors for Order Blocks.

- Increasing `ob_period`:

- Fewer levels.

- But levels tend to be more significant and reliable.

- In highly volatile markets (major news, war events, FOMC, etc.),

using values 7–10 is recommended to filter out weak levels.

- Show Fair Value Gaps (`show_fvg`)

Enables/disables the drawing of FVG zones (imbalances).

- Bullish OB Color (`c_ob_bull`)

- Color of Bullish Order Blocks (Demand Zones).

- Default: semi-transparent green (transparency ≈ 80).

- Bearish OB Color (`c_ob_bear`)

- Color of Bearish Order Blocks (Supply Zones).

- Default: semi-transparent red.

- Bullish FVG Color (`c_fvg_bull`)

- Color of Bullish FVG (upward imbalance), typically yellow.

- Bearish FVG Color (`c_fvg_bear`)

- Color of Bearish FVG (downward imbalance), typically purple.

### 2.3 Smart DCA Strategy Group

- Enable DCA Zones (`show_dca`)

Enables the Smart DCA logic and visual labels.

- RSI Length (`rsi_len`)

Lookback period for RSI (default: 14).

- Shorter → more sensitive, more noise.

- Longer → fewer signals, higher reliability.

- Bollinger Bands Length (`bb_len`)

Moving average period for Bollinger Bands (default: 20).

- BB Multiplier (`bb_mult`)

Standard deviation multiplier for Bollinger Bands (default: 2.0).

- For extremely volatile markets, values like 2.5–3.0 can be used so that only extreme deviations trigger a DCA signal.

### 2.4 Volume Profile (Visible Range Sim) Group

- Show Volume Profile (`show_vp`)

Enables the simulated Volume Profile bars on the right side of the chart.

- Volume Lookback Bars (`vp_lookback`)

Number of bars used to compute the Volume Profile (default: 150).

- Higher values → broader historical context, heavier computation.

- Row Count (`vp_rows`)

Number of vertical price segments (rows) to divide the total price range into (default: 30).

- Width (%) (`vp_width`)

Relative width of each volume bar as a percentage.

In the code, bar widths are scaled relative to the row with the maximum volume.

> Technical note: Volume Profile calculations are executed only on the last bar (`barstate.islast`) to keep the script performant even on higher timeframes.

### 2.5 Wyckoff Helper Group

- Show Wyckoff Events (`show_wyc`)

Enables detection and plotting of Wyckoff Spring events.

- Volume MA Length (`vol_ma_len`)

Length of the moving average on volume.

A bar is considered to have Ultra Volume if its volume is more than 2× the volume MA.

## Chapter 3 – Smart Money Strategy (Order Blocks & FVG)

### 3.1 What Is an Order Block?

An Order Block (OB) represents the footprint of large institutional orders:

- Bullish Order Block (Demand Zone)

The last selling region (bearish candle/cluster) before a strong upward move.

- Bearish Order Block (Supply Zone)

The last buying region (bullish candle/cluster) before a strong downward move.

Institutions and large players place heavy orders in these regions. Typical price behavior:

- Price moves away from the zone.

- Later returns to the same zone to fill unfilled orders.

- Then continues the larger trend.

In the script:

- If `pl` (pivot low) forms → a Bullish OB is created.

- If `ph` (pivot high) forms → a Bearish OB is created.

The box is drawn:

- From `bar_index ` to `bar_index`.

- Between `low ` and `high `.

- `extend=extend.right` extends the OB into the future, so it acts as a dynamic support/resistance zone.

- Only the last 4 OB boxes are kept to avoid clutter.

### 3.2 Order Block Color Guide

- Semi-transparent Green (`c_ob_bull`)

- Represents a Bullish Order Block (Demand Zone).

- Interpretation: a price region with a high probability of bullish reaction.

- Semi-transparent Red (`c_ob_bear`)

- Represents a Bearish Order Block (Supply Zone).

- Interpretation: a price region with a high probability of bearish reaction.

Overlap (Multiple OBs in the Same Area)

When two or more Order Blocks overlap:

- The shared area appears visually denser/stronger.

- This suggests higher order density.

- Such zones can be treated as high-priority levels for entries, exits, and stop-loss placement.

### 3.3 Demand/Supply Logic in the Scoring Engine

is_in_demand = low <= ta.lowest(low, 20)

is_in_supply = high >= ta.highest(high, 20)

- If current price is near the lowest lows of the last 20 bars, it is considered in a Demand Zone → positive impact on score.

- If current price is near the highest highs of the last 20 bars, it is considered in a Supply Zone → negative impact on score.

This logic complements Order Blocks and helps the Dashboard distinguish whether:

- Market is currently in a statistically cheap (long-friendly) area, or

- In a statistically expensive (short-friendly) area.

### 3.4 Fair Value Gaps (FVG)

#### Concept

When the market moves aggressively:

- Some price levels are skipped and never traded.

- A gap between wicks/shadows of consecutive candles appears.

- These regions are called Fair Value Gaps (FVGs) or Imbalances.

The market generally “dislikes” imbalance and often:

- Returns to these zones in the future.

- Fills the gap (rebalance).

- Then resumes its dominant direction.

#### Implementation in the Code

Bullish FVG (Yellow)

fvg_bull_cond = show_smc and show_fvg and low > high and close > high

if fvg_bull_cond

box.new(bar_index , high , bar_index, low, ...)

Core condition:

`low > high ` → the current low is above the high of two bars ago; the space between them is an untraded gap.

Bearish FVG (Purple)

fvg_bear_cond = show_smc and show_fvg and high < low and close < low

if fvg_bear_cond

box.new(bar_index , low , bar_index, high, ...)

Core condition:

`high < low ` → the current high is below the low of two bars ago; again a price gap exists.

#### FVG Color Guide

- Transparent Yellow (`c_fvg_bull`) – Bullish FVG

Often acts like a magnet for price:

- Price tends to retrace into this zone,

- Fill the imbalance,

- And then continue higher.

- Transparent Purple (`c_fvg_bear`) – Bearish FVG

Price tends to:

- Retrace upward into the purple area,

- Fill the imbalance,

- And then resume downward movement.

#### Trading with FVGs

- FVGs are *not* standalone entry signals.

They are best used as:

- Targets (take-profit zones), or

- Reaction areas where you expect a pause or reversal.

Examples:

- If you are long, a bearish FVG above is often an excellent take-profit zone.

- If you are short, a bullish FVG below is often a good cover/exit zone.

### 3.5 Core SMC Trading Templates

#### Reversal Long

1. Price trades down into a green Order Block (Demand Zone).

2. A bullish confirmation candle (Close > Open) forms inside or just above the OB.

3. If this zone is close to or aligned with a bullish FVG (yellow), the signal is reinforced.

4. Entry:

- At the close of the confirmation candle, or

- Using a limit order near the upper boundary of the OB.

5. Stop-loss:

- Slightly below the OB.

- If the OB is broken decisively and price consolidates below it, the zone loses validity.

6. Targets:

- The next FVG,

- Or the next red Order Block (Supply Zone) above.

#### Reversal Short

The mirror scenario:

- Price rallies into a red Order Block (Supply).

- A bearish confirmation candle forms (Close < Open).

- FVG/premium structure above can act as a confluence.

- Stop-loss goes above the OB.

- Targets: lower FVGs or subsequent green OBs below.

## Chapter 4 – Smart DCA Strategy (RSI + Bollinger Bands)

### 4.1 Smart DCA Concept

- Classic DCA = buying at fixed time intervals regardless of price.

- Smart DCA = scaling in only when:

- Price is statistically cheaper than usual, and

- The market is in a clear oversold condition.

Code logic:

rsi_val = ta.rsi(close, rsi_len)

= ta.bb(close, bb_len, bb_mult)

dca_buy = show_dca and rsi_val < 30 and close < bb_lower

dca_sell = show_dca and rsi_val > 70 and close > bb_upper

Conditions:

- DCA Buy – Smart Scale-In Zone

- RSI < 30 → oversold.

- Close < lower Bollinger Band → price has broken below its typical volatility envelope.

- DCA Sell – Overbought/Distribution Zone

- RSI > 70 → overbought.

- Close > upper Bollinger Band → price is extended far above the mean.

### 4.2 Visual Representation on the Chart

- Green “DCA” Label Below Candle

- Shape: `labelup`.

- Color: lime background, white text.

- Meaning: statistically attractive level for laddered spot entries or short exits.

- Red “SELL” Label Above Candle

- Warning that the market is in an extended, overbought condition.

- Suitable for profit-taking on longs or considering short entries (with proper confluence and risk management).

- Light Green Background (`bgcolor`)

- When `dca_buy` is true, the candle background turns very light green (high transparency).

- This helps visually identify DCA Zones across the chart at a glance.

### 4.3 Practical Use in Trading

#### Spot Trading

Used to build a better average entry price:

- Every time a DCA label appears, allocate a fixed portion of capital (e.g., 2–5%).

- Combining DCA signals with:

- Green OBs (Demand Zones), and/or

- The Volume Profile POC

makes the zone structurally more important.

#### Futures Trading

- Longs

- Use DCA Buy signals as low-risk zones for opening or adding to longs when:

- Price is inside a green OB, or

- The Dashboard already leans LONG.

- Shorts

- Use DCA Sell signals as:

- Exit zones for longs, or

- Areas to initiate shorts with stops above structural highs.

## Chapter 5 – Volume Profile (Visible Range Simulation)

### 5.1 Concept

Traditional volume (histogram under the chart) shows volume over time.

Volume Profile shows volume by price level:

- At which prices has the highest trading activity occurred?

- Where did buyers and sellers agree the most (High Volume Nodes – HVNs)?